By operating as member-owned, not-for-profit (NFP) institutions, credit unions face a unique set of treasury management challenges, especially compared to banks and building societies with far greater resources.

What’s more, credit unions are dual-regulated, meaning they must adhere to strict compliance rules set by both the Prudential Regulation Authority (PRA) and the Financial Conduct Authority (FCA). Ultimately, managing liquidity ratios, lending practices, and reporting deadlines can put significant strain on smaller credit unions with limited treasury staff.

That’s where a treasury policy can help. This short document outlines how your organisation should handle its financial resources, including cash, borrowing, investments, banking relationships, and risk.

Ultimately, a good treasury policy helps ensure sensible financial practices and clear audit trails, while keeping key stakeholders aligned when it comes to managing, investing, and lending funds.

Here, we share what a credit union treasury policy might look like (step-by-step) and discuss the benefits of implementing a robust and compliant policy framework.

Writing your credit union’s treasury policy from scratch? We’ve outlined what you might want to include and why each section is important below.

However, if you want to skip the admin, we’ve created a handy treasury policy template for credit unions. Simply click the link to grab your free copy.

Download your credit union treasury policy template here.

Your treasury policy should start with a section that outlines why the policy exists (its purpose) and what it covers (its scope).

To ensure accountability, control, and compliance, the next section of your document should clarify the treasury decision-making roles and responsibilities in your organisation, and the oversight structures (e.g., CEO, board members, audit committee chairs, etc.).

The credit union CFO will generally have the overall responsibility for approving the policy and maintaining financial oversight. However, they may choose to delegate this responsibility on a day-to-day basis to finance to ensure the policy is being followed while managing cash flow, banking, investments, and reporting.

The following section should clearly communicate the key goals of your treasury policy. These might include some or all of the following:

This is a vital part of the document, as these objectives will ultimately guide your organisation's treasury decisions and practices. This is particularly important as a member-owned NFP, as you have a duty to demonstrate transparent, community-focused financial stewardship.

In managing its financial assets, the Credit Union is exposed to the following key risks:

Credit Risk:

The risk that a financial institution, borrower, or counterparty may fail to meet its obligations, resulting in the loss of capital or interest income. The Credit Union manages this by maintaining prudent lending and investment criteria, setting clear counterparty limits, and only placing surplus funds with PRA- and FCA-authorised institutions that meet approved credit standards.

Liquidity Risk:

The risk that the Credit Union may be unable to access sufficient cash to meet members’ withdrawals or other short-term obligations, or may only be able to do so at an excessive cost. This risk is managed through careful cash flow forecasting, maintenance of minimum liquid asset ratios, and regular review of liquidity positions in line with regulatory requirements.

Operational Risk:

The risk of financial loss arising from inadequate or failed internal processes, people, systems, or external events — for example, transaction errors, reconciliation issues, or system failures. The Credit Union mitigates this through strong internal controls, segregation of duties, staff training, and regular internal and external audits.

Counterparty Risk:

The risk that a financial institution or other party with whom the Credit Union has entered into a financial arrangement (such as a deposit or investment) may default on its obligations. This is managed by applying strict counterparty due diligence, adhering to regulatory limits on exposures, and regularly reviewing the financial health and creditworthiness of all counterparties.

The counterparty risk section of the policy document outlines how your credit union should manage the risk of financial loss if a bank or financial institution fails to meet its obligations. In other words, how do you protect your organisation’s money against loss if a bank collapses?

This might be a pledge to only use approved, reputable institutions (such as those with strong credit ratings) or to regularly review the financial health and ratings of counterparties to ensure optimal financial stability.

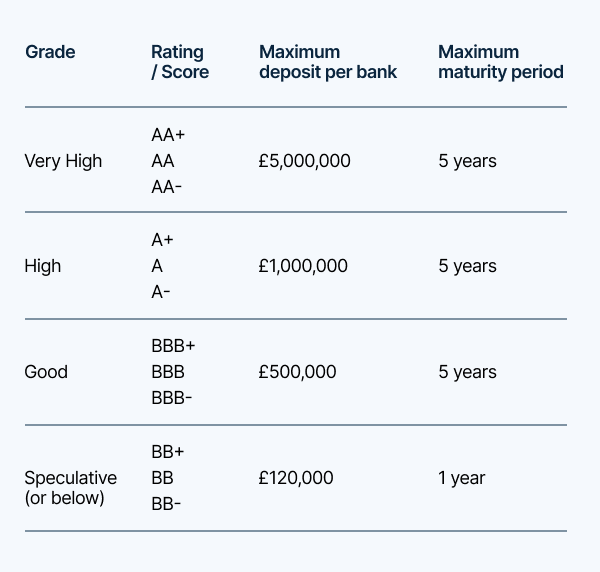

This part of your policy document should set maximum exposure levels to any single bank or financial institution to help reduce risk. The aim here is to avoid over-reliance on any one provider, protecting funds from potential financial losses.

For example, you may want to specify limits on the amount that can be deposited with an approved counterparty, or base those limits on factors such as credit rating, account type, or term length (as shown in the table above).

Join leading UK not-for-profits using our platform to earn more interest on their savings.

With a single application, your organisation can access a wide selection of competitive savings accounts from our carefully chosen banks and building societies.

Broaden your access to deposit accounts through a single application, helping you generate more interest on your savings and grow your funds without adding to your administrative workload. See how it works.

.png)

Including a reference chart comparing credit ratings from major agencies (for example, Standard & Poor’s (S&P), Moody’s, and Fitch) can help your treasury staff assess the financial strength of counterparties. These are known as “financial implied credit scores”, and they differ from traditional credit scores as they use current and historical economic data to project future credit risk — unlike scores from a credit reference agency, which look at past behaviour to determine future risk.

This chart also gives staff an at-a-glance table to:

This section of the policy document should outline how your credit union makes sure it has sufficient cash reserves to meet its financial obligations (regulatory minimums).

In short, the responsible person (e.g., CFO, finance director, or operations manager) should monitor and forecast short- and long-term cash flow, maintain a minimum cash balance for operational needs, and align investments with the expected timing of payments. You must ensure your credit union maintains a healthy buffer to absorb potential losses, protect members’ savings, and remain solvent under stress.

This section describes the types of financial instruments the credit union is allowed to invest in. You may want to include:

The aim is to protect capital, ensure accessibility, and earn a return within an acceptable level of risk.

Following on from the previous section, this part of the policy outlines how and by whom investment decisions are made.

It should clearly state who is responsible for making decisions (e.g., finance director, finance committee, or senior management) and the criteria required to ensure investments meet safety, liquidity, and return objectives.

Essentially, approved procedures must be followed to ensure all investment decisions are prudent, transparent, and accountable.

This is an optional section that you may want to include, depending on your credit union’s commitment to ethical and responsible financial practices.

Note: This part hasn’t been included in our treasury policy template.

If you want to align your treasury decisions with your organisation’s values and mission, having ESG investment criteria can help ensure that your organisation’s surplus funds don’t support activities that conflict with its member values and community orientation.

Key elements may include:

.png)

For more insights into the ethics of different UK banks, read the Ethical Consumer's Bank Guide.

The penultimate part of your treasury policy outlines how you’ll track and review treasury activities to ensure compliance, performance, and transparency.

You may want the report to include:

This report might be produced monthly, quarterly, or when requested.

Finally, the document should conclude with a commitment to review the policy to ensure it’s still fit for purpose. This is typically done annually, but you can also decide to review things when there are significant changes (e.g. in regulations or to financial strategy).

There are several benefits to implementing a treasury policy in a credit union, including:

Create your own treasury policy: Download your free example template

Now you know what you need to include in your organisation’s treasury policy (and why it matters), you can create one from scratch — or grab a ready-made template from Insignis.

Feel free to adapt and modify the language and template according to your credit union’s structure, governance framework, and regulatory environment. Please ensure that it is reviewed by a financial or legal professional before publishing. This template is provided for general guidance only. We accept no responsibility or liability for its use, whether in its original form or after modification.

Ready to strengthen your credit union's financial governance? Download our free treasury policy example to guide your next policy update.

8 Devonshire Square, London EC2M 4YJ

St John’s Innovation Centre, Cowley Rd, Milton, Cambridge CB4 0WS

+44 (0)1223 200 674