The UK’s Financial Services Compensation Scheme (FSCS) protects eligible customers of authorised financial institutions by paying compensation of up to £120,000 in the event of collapse.

The scheme gives banking customers peace of mind that their cash deposits are safe (up to a limit) in case the worst happens.

But does FSCS protection extend to business accounts? The short answer is that it could. Whether or not your deposits are eligible may be a little more complicated.

To help you get to grips with the FSCS for businesses, in this article we:

The UK government’s Financial Services Compensation Scheme allows sole traders, limited companies, and partnerships to claim compensation of up to £120,000 per institution if their bank, building society, or credit union fails and cannot repay the money itself (in other words, it is in default).

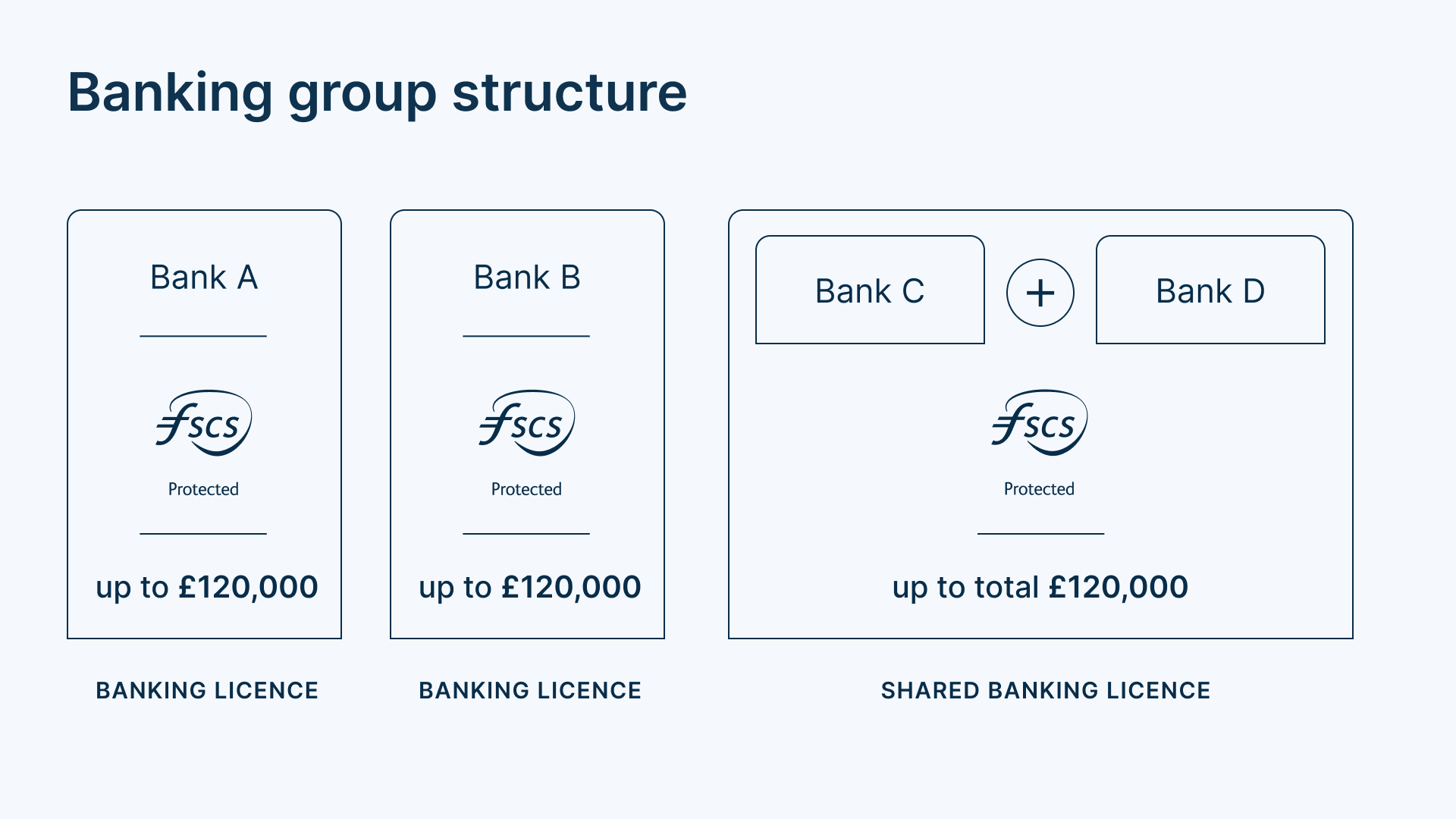

Note: The £120,000 limit applies to all accounts held with institutions that operate under the same licence; therefore, to optimise FSCS coverage, larger deposits should be placed with institutions that form part of separate or independent groups.

The scheme protects most businesses, regardless of size, number of employees, or turnover. However, eligibility is assessed on a case-by-case basis.

If you’re a small business owner, you can check if you can claim on the FSCS website. It’s free to make a claim — and if your business is eligible, it’ll get 100% of the money owed (subject to the £120,000 limit) and won’t be charged any fees.

The FSCS covers various financial products for businesses, including:

The FSCS generally protects a business’s cash deposits, regardless of company size. If a bank, building society, or credit union fails, the scheme will automatically compensate each eligible company depositor up to £120,000. This applies to financial institutions that failed after January 2017.

However, things can become a little more complex depending on how your business is structured. For example:

It’s also worth noting that each person is entitled to the £120,000 limit for personal joint accounts, meaning that £240,000 in total can be claimed. However, this does not apply to business partnerships. If a joint business account is held by two or more business partners, it’s still only covered up to £120,000.

Note: Your business bank account provider must be authorised by the Prudential Regulation Authority to qualify for protection. Use the FSCS’s bank and savings protection checker tool to see if your provider is covered.

If you paid for business cover with an insurer that has failed, you may be able to claim compensation from the FSCS, provided your company has an annual turnover of less than £1 million.

To be eligible for protection, the insurer must have been regulated by the Prudential Regulation Authority (PRA).

If you’ve invested in pension funds, stocks, or bonds through your company, you may be able to claim compensation worth up to £120,000 should the provider or adviser go out of business. This applies to firms that failed after 1 April 2019.

However, to qualify for this protection, your business must meet the criteria of a “small company” under section 382 of the Companies Act 2006. There are three criteria: annual turnover, balance sheet, and number of employees. Your firm must meet two of the three to qualify as “small” (see below).

Furthermore, the provider must have been authorised by the Financial Conduct Authority (FCA) or Prudential Regulation Authority (PRA) at the time of failure.

The compensation scheme exists to protect you when a financial institution fails. You won’t be covered against loss of income caused by market fluctuations, fraud, or your own negligence.

You don’t have to look too far into the past to find an example of the importance of diversifying funds. The 2023 collapse of Silicon Valley Bank (SVB) offers a stark reminder of the real-world risks of exposure to a single bank and the lack of protection this provides.

What’s more, it proves just how quickly things can unravel.

SVB collapsed due to structural vulnerabilities in its business model, which were exposed when rising interest rates and concentrated withdrawals from its tech-focused client base triggered a run on the bank, with depositors withdrawing more than $42 billion in a single day.

Silicon Valley Bank failed in less than a week, meaning its UK subsidiary (SVB UK) collapsed. Fortunately, the FSCS protected deposits at SVB UK up to £85,000 per eligible depositor. However, you could have faced significant losses if you had held more than the £85k limit at the time of collapse and couldn’t withdraw your cash in time.

The lesson from the SVB bank run and subsequent failure is that market volatility can affect cash, too. Diversification is a critical cash management strategy.

A cash management platform like Insignis can help diversify your business cash holdings, mitigate risk, and optimise your FSCS protection where eligible. Get started here.

In most cases, you don’t even need to apply; the FSCS will automatically compensate you, typically within seven days for deposits.

However, the FSCS website makes it easy to claim online for more complex cases. You can do so in three simple steps:

According to the FSCS website, completing the online application can take 1-2 hours. You can save your progress and return at any time.

Find out more about the FSCS claims process here.

Business owners, Finance Directors, and CFOs are responsible for understanding FSCS protection criteria and effectively managing their company’s cash reserves.

To recap, if your business is eligible, up to £120,000 is protected per authorised financial institution, and each must have its own banking licence to qualify for complete protection (in other words, if you have multiple accounts across different banks, they cannot be in the same banking group).

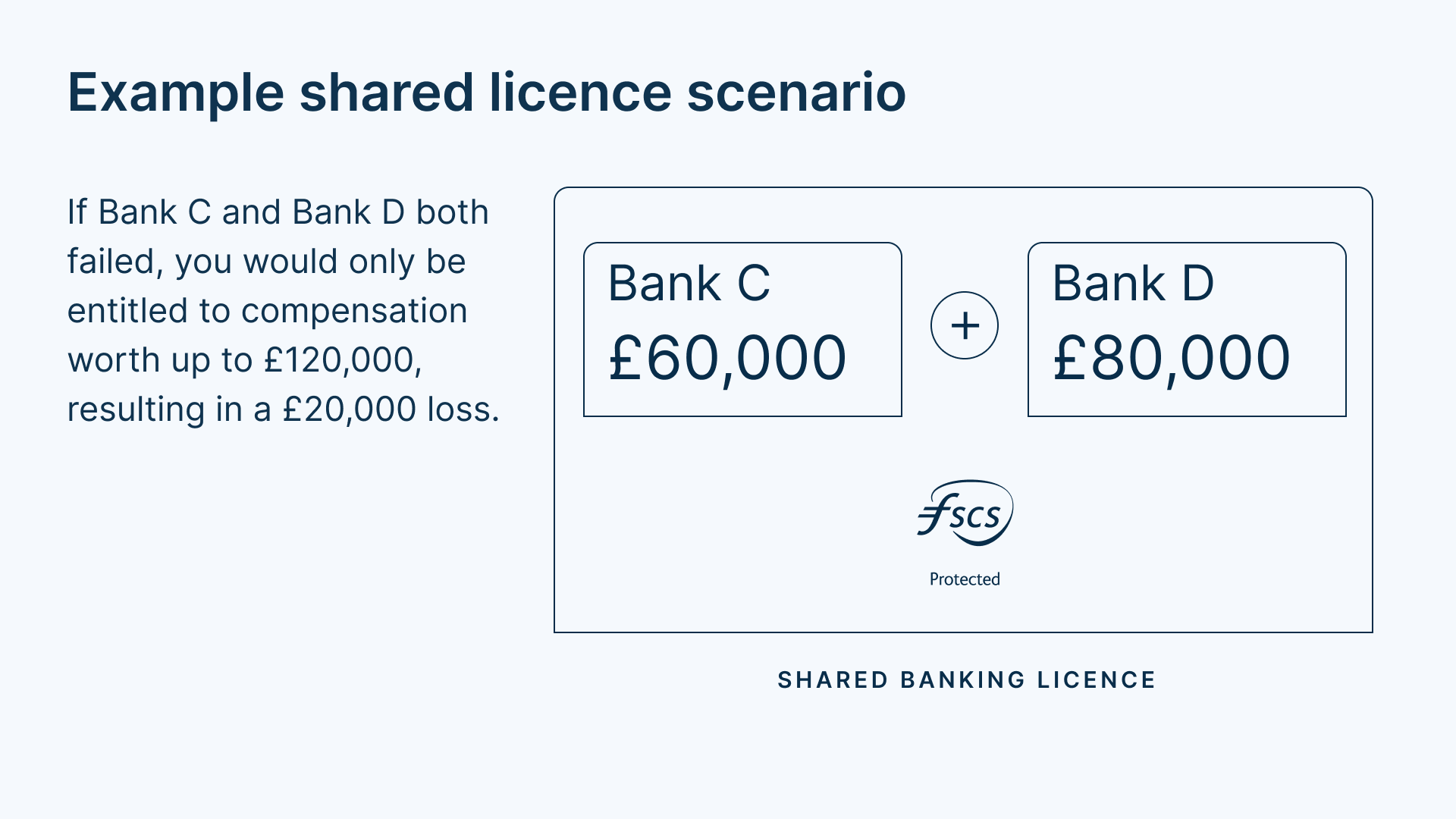

To see how this might affect your business, consider the following scenario:

You’re the director of a limited company, and your business has accounts with Bank C (£60,000 balance) and Bank D (£80,000 balance). These banks, while distinct brands, share a banking licence. The banks fail, and because they’re part of the same group, they’re treated as the same bank for FSCS purposes. This means you’d only be entitled to compensation worth up to £120,000, resulting in a £20,000 loss.

Diversifying your cash reserves and spreading the risk by opening several savings accounts with banks and building societies with distinct licences can help you manage and protect your company’s money.

This might seem time-consuming with stacks of paperwork, not to mention a headache to administer — but it doesn’t have to be.

With Insignis’ single sign-up process, you can access exclusive rates and hundreds of business deposit accounts from over 55 banks and building societies.

With easy access, short-term notice and fixed-term accounts, you can capitalise on liquidity events and withdraw funds precisely when your business requires them, optimising FSCS protection subject to eligibility through efficient bank diversification.

Find out more about our business accounts here.

8 Devonshire Square, London EC2M 4YJ

St John’s Innovation Centre, Cowley Rd, Milton, Cambridge CB4 0WS

+44 (0)1223 200 674