The right place to put savings depends on various factors, including the amount you’ve saved, your risk appetite and objectives, and whether you need regular access to the money.

For growing wealth, higher-risk investment options, such as stocks, potentially offer larger returns. But you’re also at risk of losing some or all of your initial capital (in this case, if the stock price plunges). Additionally, you can’t always withdraw cash in investments on short notice.

While depositing your cash in a savings account does not put your capital at risk, the trade-off is modest returns that may not keep pace with inflation. Splitting your savings across various financial products can help you strike a balance between risk and return.

In this article, we discuss:

Certain factors that you may want to consider when deciding between keeping your money in savings and investing it, and the potential benefits of maintaining a diversified portfolio.

5 types of savings accounts and 4 types of investment products, with the pros and cons associated with each.

Disclaimer: The information provided in this article is for informational purposes only and does not constitute financial, investment, or professional advice. Insignis is not authorised to offer financial advice, and the information shared should not be relied upon when making financial decisions. For guidance tailored to your personal circumstances, please consult a qualified financial adviser.

Evaluating financial products: key considerations

Risk, returns, and ease of access aren’t the only important considerations for where you put your savings. It’s also essential to account for:

Security: Even low-risk options, such as savings accounts, aren’t 100% secure. If the bank or building society with which you have an account collapses, you could lose your money. The Financial Services Compensation Scheme (FSCS) offers protection for the capital you invest in several types of financial products, including savings accounts, mortgages, funeral plans, insurance, and more. If you hold money in a UK-authorised bank, building society, or credit union, FSCS covers up to £85,000 (per person, per institution).

Tax implications: The income you earn from your savings —like via interest or dividends—may be taxable. Some financial products shield your savings income from taxes, like pensions and ISAs. High-net-worth individuals will often split their wealth across various tax-sheltered products.

Stress: Some investments can be stressful, and for different reasons—managing them might require effort, or their volatility can result in uncertainties about potential returns. For example, buying a rental property involves maintenance and tenant management, while stock values will fluctuate over time. When deciding where to invest, consider the convenience of various options and the potential stress associated with owning them.

If you have a considerably large savings pot—tens of thousands or hundreds of thousands of pounds—then it’s worth considering portfolio diversification. Spreading your savings across different financial products offers several potential advantages.

These may include:

Balancing risk and returns: Diversifying your savings across products with different risk and return profiles can increase the overall return potential while mitigating risk. For example, if you invested portions of your savings in a fixed-rate savings account, stocks and shares, and a pension, you’d theoretically take on less risk than only buying stocks. You’d also have a higher potential for returns than if you only invested in a savings account.

Maximising your FSCS coverage: To keep more than £85,000 in savings accounts with minimal risk, you’ll need to spread it across more than one account with institutions that have distinct licenses to maximise FSCS coverage. For the purposes of FSCS coverage, banks or building societies in the same group are considered as one entity. This means if you deposit money into accounts by different banks in the same group, you’ll only be covered for £85,000.

Benefit from different terms: Spreading your money across financial products can give you more flexibility and make balancing short- and long-term goals easier. For example, you could keep some cash in an easy-access savings account for your emergency fund, invest some in stocks, and shelter some from taxes in a pension. Since pensions and ISAs have limits on how much tax relief you’ll receive or how much you can pay into them each year, you’ll need to consider multiple financial products if you have a large savings pot.

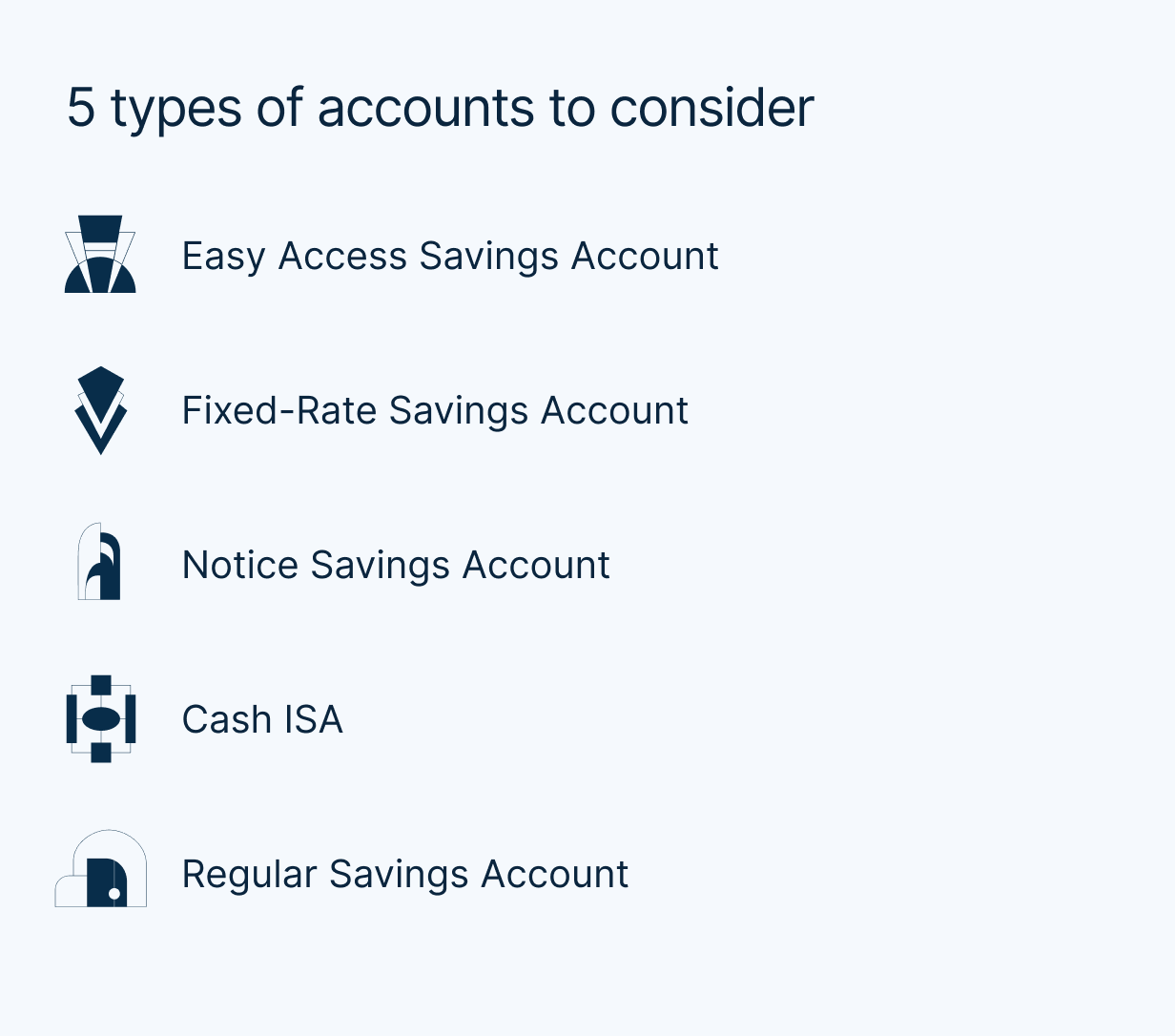

If you plan to keep all or some of your savings in cash, you can choose from several savings accounts with different terms and interest rates:

Easy Access Savings Account. These are a good choice for emergency funds, rainy day funds, or if you just want the flexibility that comes with being able to access your funds on demand. The downside of these accounts is that they attract lower, variable interest rates. These rates don’t typically keep up with inflation, and their variability makes returns less predictable.

Fixed-Rate Savings Account. Thanks to their relatively higher interest rates, fixed-rate accounts offer greater returns than an easy-access account. You’ll usually get the best interest rates on accounts with longer fixed terms—it’s worth checking the rates and fixed periods offered by different providers. At the very least, it’s best to ensure the rates keep up with (and ideally outpace) projected inflation.

Notice Savings Account. If you’re put off by the low interest rates offered by easy access accounts, but aren’t keen on locking your money away, then a notice savings account is a good middle ground. A notice account is a type of savings account that requires you to give advance notice, dependent on the advertised "notice period", before you can withdraw your money. Be sure to compare account terms to find one that suits your needs; notice periods, withdrawal limits, and interest rates are the main factors to consider. Similar to fixed-rate accounts, notice accounts with the longest notice periods usually offer the best interest rates.

Cash ISA. Individual Savings Accounts (ISAs) are an option for shielding savings from taxes, subject to the application of an annual allowance, which is £20,000 for the current tax year. You can open and pay into multiple ISAs in the same tax year subject to the annual allowance.

Regular Savings Account. These accounts are worth considering if you’re looking to deposit a fixed monthly amount and benefit from top interest rates. However, they’re less appealing for investing lump sums of money because of savings limits and stringent terms (e.g., limited withdrawals). Also, as you deposit money monthly, your full balance isn’t earning interest for the entire year. Consequently, as your average balance over the year is lower than the final total, you will learn less in interest over the year than the quoted account rate.

4 financial products you might consider for growing your money

Stocks and shares. Stocks and shares have the potential to offer some of the highest returns, making them an attractive choice for growing wealth. Buying stocks by paying into a professional fund can help you balance the overall investment risk. Investment managers will usually spread your investment across different stocks, and they’ll brief you on the overall risk and earnings potential.

Investment bonds. Investment bonds offer higher returns than cash savings, but are typically lower-risk than investments in the stock markets. When you approach an organisation (usually a life insurance company) about buying investment bonds, they should tell you about the various funds your money will be invested in. The returns potential across different funds varies, and it’s not uncommon for the value of your investment to fluctuate over time.

Pensions. Pensions are helpful for more than saving for retirement—they’re a promising option for sheltering taxes and growing your money. When you contact a private pension provider, they should ask about your risk appetite and recommend customised options accordingly. It’s essential to understand the fund’s historical performance, how your money will be invested, and any management fees that apply. Don’t forget that you can’t access the money in your pension until you turn 55 (or 57, if you were born after 1971).

Children’s Pensions. Children’s pensions let you shelter more of your money from taxes and grow wealth for your children’s futures. Just like adult pensions, the UK government pays money equivalent to 20% of eligible contributions into your child’s pension each tax year. A total of £2,880 can be deposited per tax year into the pension, meaning the government contributes £720 if you hit the limit.

Discover and compare different savings products with ease using Insignis

If you’re interested in putting your money in savings products, you can use Insignis to find accounts that meet your needs and preferences. Insignis eliminates the manual work involved in searching for and comparing different savings products. No more scouring the market, consulting comparison sites, or tracking interest rate trends.

Our award-winning platform gives you access to:

Over 3,500 savings products from 50+ banks and building societies

Competitive interest rates

Effortless savings management

Optimised FSCS coverage

Don’t sit on it, Insignis it. Ask your financial adviser about Insignis today.

You may be interested in these articles as well...